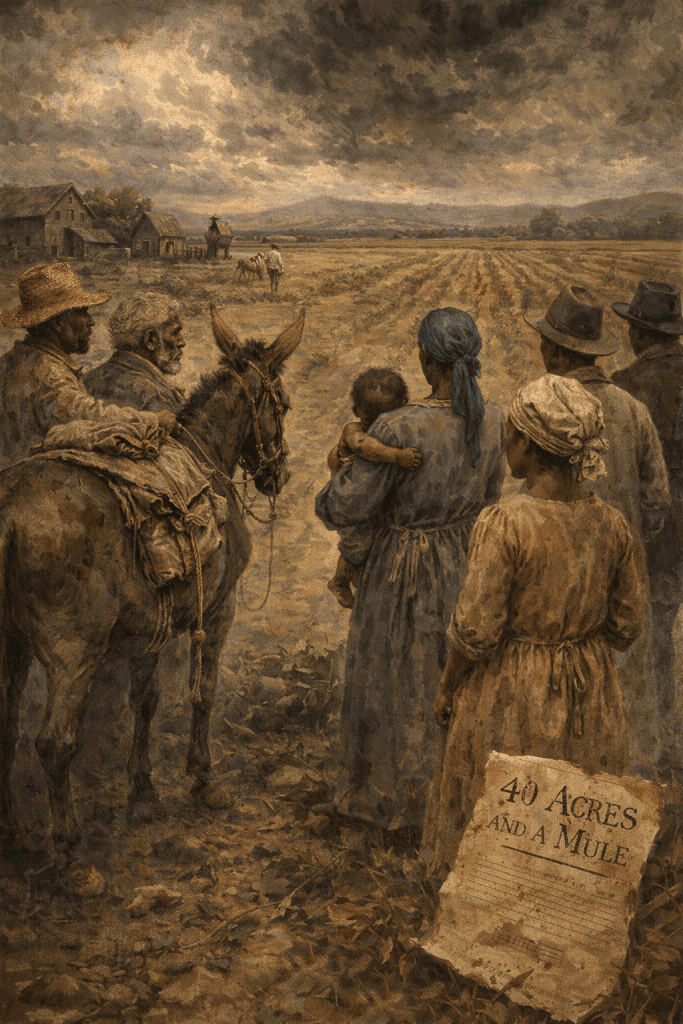

The phrase “40 acres and a mule” has become one of the most powerful symbols of broken promises in American history, rooted in the aftermath of the American Civil War. It represents an unfulfilled commitment to provide formerly enslaved Black Americans with land and the means to sustain themselves economically.

The origin of this promise can be traced to January 1865, when Union General William Tecumseh Sherman issued Special Field Orders No. 15. This order set aside approximately 400,000 acres of confiscated Confederate land along the southeastern coast for settlement by freed Black families.

Under Sherman’s directive, each family was to receive up to 40 acres of land. Later, some were also given access to surplus army mules, leading to the enduring phrase “40 acres and a mule.” This initiative was seen as a foundational step toward economic independence.

The policy was implemented in areas of South Carolina, Georgia, and Florida, where thousands of formerly enslaved people began to establish communities. For many, this land represented not just property, but dignity, autonomy, and the fruit of generations of unpaid labor.

The idea of land redistribution was supported by leaders such as Thaddeus Stevens, who argued that true freedom required economic justice. Without land, formerly enslaved people would remain dependent on their former oppressors.

However, this promise was short-lived. Following the assassination of Abraham Lincoln in April 1865, his successor, Andrew Johnson, reversed many Reconstruction policies.

President Johnson issued proclamations that returned confiscated land to former Confederate landowners. As a result, thousands of Black families who had begun to build lives on this land were forcibly removed.

This reversal effectively nullified the promise of “40 acres and a mule.” Land that had been distributed to freedmen was taken back, often violently, leaving families dispossessed and vulnerable.

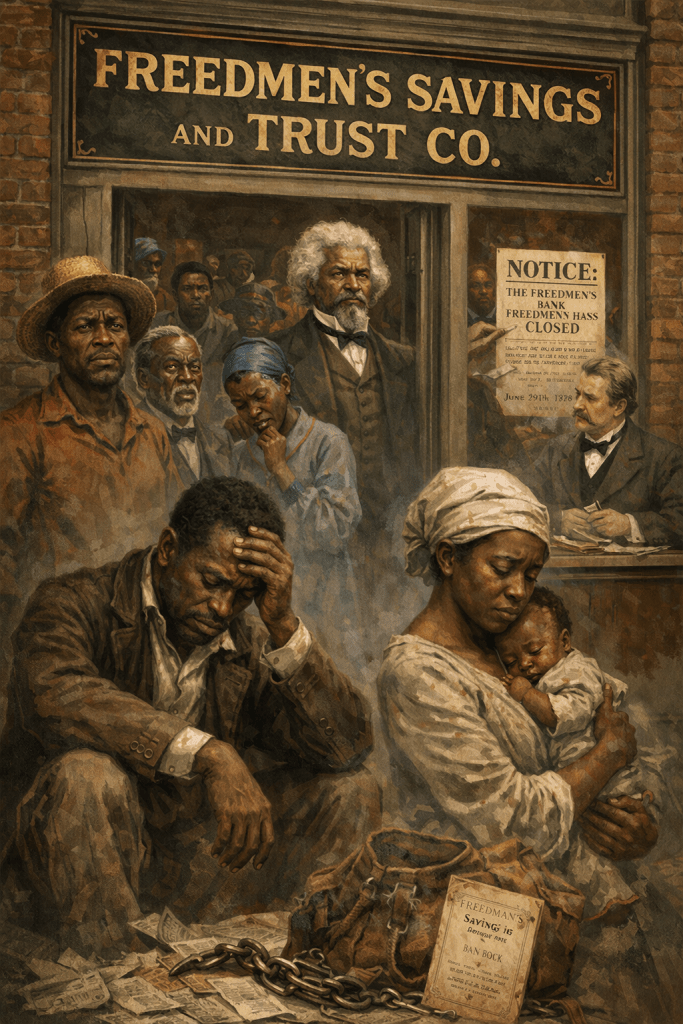

The failure to provide land had profound consequences. Without access to property, many Black Americans were pushed into sharecropping—a system that closely resembled slavery in its economic exploitation.

Sharecropping trapped families in cycles of debt and poverty. Landowners controlled the terms, often charging exorbitant fees for tools, seeds, and housing, ensuring that laborers remained financially dependent.

The denial of land ownership also prevented the accumulation of generational wealth. While white Americans were able to pass down land and assets, Black families were systematically excluded from these opportunities.

The concept of reparations is deeply tied to this history. Advocates argue that the promise of land was a form of restitution for centuries of slavery, and its revocation constitutes a debt still owed.

The economic disparity created by this broken promise is evident today. Scholars frequently link the racial wealth gap to the lack of land redistribution during Reconstruction.

The federal government’s failure to uphold its commitment undermined trust and reinforced systemic inequality. It demonstrated that legal freedom without economic support was insufficient.

In the 20th and 21st centuries, the call for reparations has gained renewed attention. Proposals include financial compensation, land grants, and institutional investments in Black communities.

Legislative efforts such as H.R. 40—named in reference to the original promise—seek to study and develop reparations proposals. The bill symbolizes a continued demand for accountability and justice.

Critics of reparations often argue against revisiting the past, but proponents emphasize that the effects of slavery and Reconstruction policies are still present in modern society.

The story of “40 acres and a mule” is not just historical—it is a living legacy that shapes economic realities today. It highlights the intersection of race, policy, and wealth in America.

Understanding this history is essential for addressing contemporary inequalities. It reveals how systemic decisions made over a century ago continue to impact generations.

The promise of land represented more than compensation—it was an opportunity for true independence. Its denial ensured that freedom would remain incomplete for millions.

Ultimately, “40 acres and a mule” stands as a reminder that justice delayed is justice denied. It calls for a reckoning with the past and a commitment to building a more equitable future.

References

Foner, E. (1988). Reconstruction: America’s Unfinished Revolution, 1863–1877. Harper & Row.

Gates, H. L. (2013). Life Upon These Shores: Looking at African American History, 1513–2008. Knopf.

Oubre, C. (1978). Forty Acres and a Mule: The Freedmen’s Bureau and Black Land Ownership. Louisiana State University Press.

Painter, N. I. (2007). Creating Black Americans: African-American History and Its Meanings, 1619 to the Present. Oxford University Press.

Williamson, J. (1995). After Slavery: The Negro in South Carolina During Reconstruction, 1861–1877. University of North Carolina Press.