Saving money is not merely a financial exercise; it is a discipline that reflects wisdom, foresight, and self-governance. In a society driven by consumption and instant gratification, the ability to save distinguishes those who plan for stability from those trapped in cycles of financial stress. Money-saving habits build resilience, protect families, and create opportunities for long-term growth rather than short-term pleasure.

One of the most foundational money-saving principles is intentional budgeting. A budget is not a restriction but a framework that assigns purpose to every dollar. When individuals track income and expenses, they gain clarity over spending patterns and identify areas of waste. Research consistently shows that people who budget regularly are more likely to achieve financial goals and avoid unnecessary debt.

Living below one’s means is a timeless financial strategy. This principle encourages spending less than what is earned, regardless of income level. Lifestyle inflation, where spending rises alongside income, is a major obstacle to wealth-building. Choosing modest living arrangements and controlled spending allows surplus income to be directed toward savings and investments.

Emergency savings are a critical pillar of financial security. Unexpected expenses such as medical bills, car repairs, or job loss can destabilize households without adequate reserves. Financial experts recommend setting aside three to six months of living expenses. This buffer reduces reliance on high-interest credit and provides peace of mind during crises.

Reducing discretionary spending is one of the quickest ways to save money. Small daily expenses—coffee purchases, food delivery, subscription services—may seem insignificant individually but accumulate substantially over time. By preparing meals at home and evaluating recurring expenses, individuals can redirect hundreds or thousands of dollars annually toward savings.

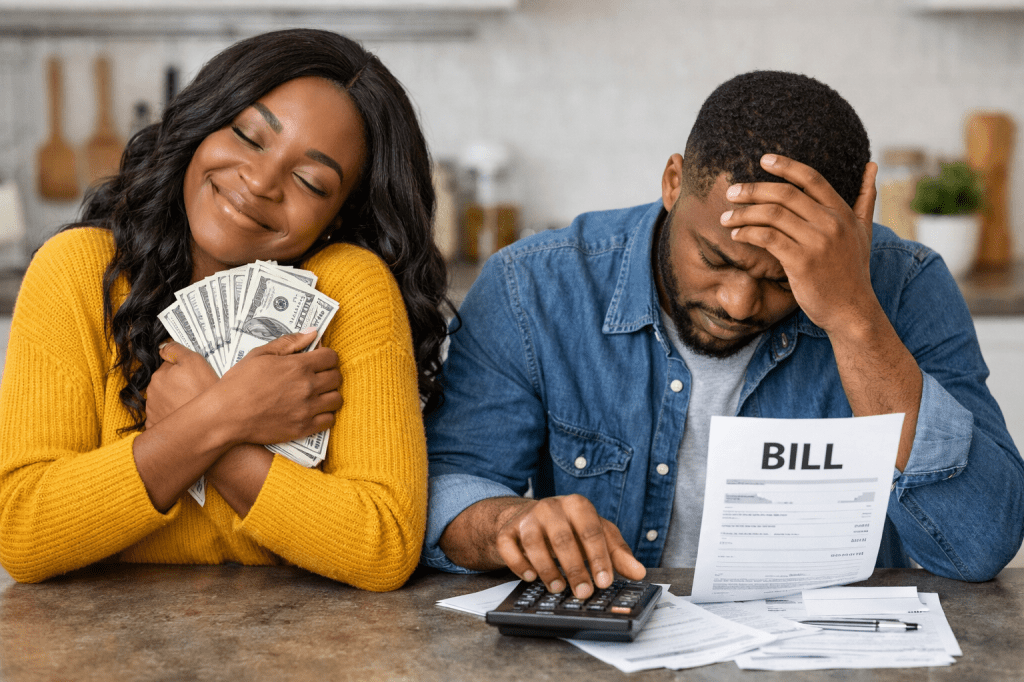

Debt management plays a vital role in money-saving strategies. High-interest debt, particularly credit card debt, erodes financial progress by compounding rapidly. Paying down balances aggressively and avoiding unnecessary borrowing frees income for saving and investing. Scripture warns that “the borrower is servant to the lender” (Proverbs 22:7, KJV), emphasizing the burden debt places on financial freedom.

Delayed gratification is a powerful yet undervalued saving tool. The ability to wait before making purchases reduces impulse buying and encourages thoughtful decision-making. Studies in behavioral economics show that individuals who practice delayed gratification are more likely to accumulate wealth and achieve long-term financial success.

Automating savings removes emotional decision-making from the process. Automatic transfers to savings or retirement accounts ensure consistency and discipline. When savings occur before spending, individuals adapt to living on the remainder rather than saving what is left over.

Shopping with intention also contributes significantly to savings. Comparing prices, using shopping lists, and avoiding emotional purchases help control spending. Retail marketing is designed to trigger impulse buying, making awareness and restraint essential financial skills.

Housing costs are often the largest household expense, making them a critical focus area. Choosing affordable housing relative to income can dramatically improve saving capacity. Downsizing, refinancing, or relocating to lower-cost areas may offer long-term financial benefits.

Transportation expenses can quietly drain finances. Opting for reliable used vehicles instead of new ones, minimizing car loans, and maintaining vehicles properly reduces long-term costs. New cars depreciate rapidly, making them one of the least effective uses of borrowed money.

Energy efficiency is an often-overlooked saving opportunity. Simple measures such as reducing energy consumption, using efficient appliances, and monitoring utility usage can lower monthly bills. Over time, these small adjustments compound into meaningful savings.

Financial literacy empowers better saving decisions. Understanding interest rates, inflation, and opportunity cost allows individuals to recognize how money grows or shrinks over time. Education reduces vulnerability to predatory financial practices and promotes long-term stability.

Setting clear financial goals strengthens saving motivation. Whether saving for homeownership, education, retirement, or generational wealth, defined goals provide direction and accountability. Goals transform saving from a vague intention into a purposeful act.

Spiritual wisdom also supports financial stewardship. The Bible emphasizes prudence, preparation, and self-control in financial matters. “Go to the ant… consider her ways, and be wise” (Proverbs 6:6, KJV) highlights diligence and preparation as virtues tied to provision.

Contentment is a powerful antidote to overspending. Modern culture promotes comparison and status consumption, which undermine saving efforts. Learning to appreciate what one has reduces the pressure to spend for validation and allows money to serve genuine needs rather than ego.

Teaching children money-saving habits strengthens generational financial health. Early exposure to budgeting, saving, and delayed gratification shapes lifelong financial behavior. Families that discuss money openly are better equipped to break cycles of financial instability.

Long-term saving should also include retirement planning. Contributing early to retirement accounts leverages compound interest, one of the most powerful wealth-building mechanisms. Even modest, consistent contributions can produce substantial outcomes over time.

Money-saving is ultimately about freedom and alignment with values. Savings provide the ability to give, invest, and respond to life’s challenges without panic. Financial discipline supports personal dignity and communal responsibility.

In conclusion, money-saving tips are not isolated tactics but interconnected habits rooted in wisdom, discipline, and intentional living. By combining practical financial strategies with ethical and spiritual principles, individuals can build stability, reduce stress, and create a future marked by stewardship rather than scarcity.

References

Baker, H. K., & Ricciardi, V. (2014). Investor behavior: The psychology of financial planning and investing. Wiley.

Lusardi, A., & Mitchell, O. S. (2014). The economic importance of financial literacy: Theory and evidence. Journal of Economic Literature, 52(1), 5–44. https://doi.org/10.1257/jel.52.1.5

Ramsey, D. (2013). The total money makeover. Thomas Nelson.

Thaler, R. H., & Sunstein, C. R. (2008). Nudge: Improving decisions about health, wealth, and happiness. Yale University Press.

The Holy Bible, King James Version. (1769/2017). Cambridge University Press.